Inheritance Wonder: Can an Estate Own a Business?

Have you ever wondered what happens to a business when its owner passes away? Can an estate legally own a sole proprietorship business? These are questions that many people may have never considered, but they are important ones to think about when planning for the future.

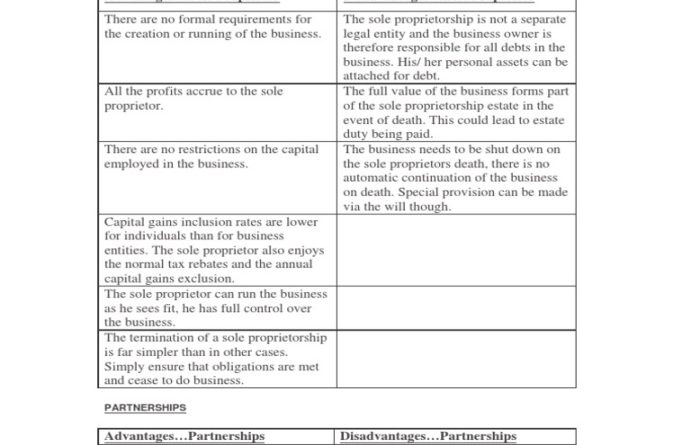

When an individual passes away, their assets and liabilities become part of their estate. This includes any businesses that the individual owned as a sole proprietor. In the case of a sole proprietorship, the business is not a separate legal entity from the owner. This means that when the owner dies, the business technically dies with them.

However, in some cases, the business can continue to operate under the ownership of the estate. This can happen if the deceased owner had a will that specified what should happen to the business upon their death. In this scenario, the business becomes an asset of the estate and can be managed or sold according to the terms of the will.

If the deceased owner did not have a will, the business would typically pass to their heirs according to the laws of intestate succession. This means that the business would be divided among the owner’s closest living relatives, such as their spouse, children, or parents. In this case, the estate would still technically own the business until it is transferred to the heirs.

There are also legal and logistical considerations to take into account when an estate owns a business. For example, the executor of the estate may need to apply for an employer identification number (EIN) for the business in order to file taxes and handle other financial matters. The executor may also need to obtain any necessary licenses or permits to continue operating the business legally.

In some cases, the executor may decide that it is in the best interest of the estate to sell the business rather than continue operating it. This can be a complex process that requires careful planning and consideration of the business’s value and marketability. The proceeds from the sale of the business would then become part of the estate and be distributed to the heirs according to the terms of the will or intestate succession laws.

Overall, the question of whether an estate can legally own a sole proprietorship business is a nuanced one that depends on a variety of factors, including the owner’s estate planning documents, the laws of intestate succession, and the decisions of the executor of the estate. While it is possible for an estate to own and operate a business, it is important to seek legal guidance to ensure that all necessary steps are taken to protect the business and the interests of the heirs.

Exploring the Legal Possibilities for Sole Proprietorships

When it comes to the world of business ownership, there are various structures that one can choose from. One of the most common and simplest forms of business ownership is a sole proprietorship. In a sole proprietorship, an individual owns and operates the business on their own, without any formal legal entity separate from themselves.

But what happens if the owner of a sole proprietorship passes away? Can their estate legally own the business? This question raises some interesting legal possibilities that are worth exploring.

In most cases, when the owner of a sole proprietorship passes away, the business is considered a part of their estate. This means that the business assets, liabilities, and operations become the responsibility of the estate. However, whether or not the estate can legally continue to operate the business as a sole proprietorship depends on a few factors.

One factor to consider is whether the deceased owner had any specific provisions in their will regarding the business. If the will clearly states that the business is to be continued by the estate, then it is possible for the estate to legally own and operate the business as a sole proprietorship.

Another factor to consider is the legal requirements in the jurisdiction where the business is located. Some states may have specific laws or regulations that govern the transfer of ownership of a sole proprietorship upon the death of the owner. In some cases, the estate may need to go through a legal process to transfer ownership of the business.

It is also important to consider the practical implications of having an estate own a sole proprietorship. Since a sole proprietorship is essentially an extension of the owner, it may not be ideal for the estate to continue operating the business in the same manner. The estate may need to hire a new manager or executor to oversee the operations of the business, which can add an extra layer of complexity.

Alternatively, the estate may choose to sell the business or dissolve it altogether. Selling the business can help the estate generate funds to pay off any debts or distribute assets to beneficiaries. Dissolving the business may be necessary if there are no interested parties to take over the operations.

In conclusion, while it is possible for an estate to legally own a sole proprietorship business, there are various factors to consider. From legal requirements to practical implications, the decision to have an estate continue operating a sole proprietorship should be carefully thought out. Ultimately, the goal is to ensure that the business assets are properly managed and that any obligations are fulfilled in accordance with the law.

Can An Estate Own A Sole Proprietorship Business